🔍Company Deep Dive #3 - $BABA (Alibaba)

It is surprising how little the market values such a huge company.

◆What is Alibaba?

Alibaba Group is an e-commerce giant in China, some might even say it is the biggest online retailer platform in the world. Although it has expanded its business segments throughout the years, its primary revenue stream still lies heavily on its digital retail and wholesale business. Its three main sites — Taobao, Tmall, and Alibaba.com, from which hundreds of millions of users shopped online around the world, had generated 88% of its revenue as reported in Q3 FY 2021.

Just like Amazon and Facebook which are still undergoing antitrust probes on the US soil, the fast-growing company had also faced more and more regulatory pressure from its government in recent years, although in this case, the odds had mostly been against Alibaba. Unlike its US rivals, Alibaba is faced with a harsher regulatory environment where the Chinese government has more authoritarian control over the tech companies. Because of that, the stock price had been in free fall from its 52-weeks-high ever since its subsidiary company Ant Group’s IPO was suspended by the Chinese government last year. Recently, the company also made headlines after being fined $2.8 Billion on monopoly practices by the Chinese government.

In this day and age where most tech stocks are already overbought by some measures, $BABA is one of the few which I believe might actually be in a sweet spot today, especially for value investors who crave some high growth yields in their portfolio. Don’t just take it from me, Charlie Munger who had not made any changes to its portfolio — Daily Journal Corp since 2014 had just purchased 165,320 shares of Alibaba recently, as disclosed in his 13F filing for Q1 2021. What did he possibly see in the company that the rest of Wall St didn’t? Let’s take a deep dive into the company.

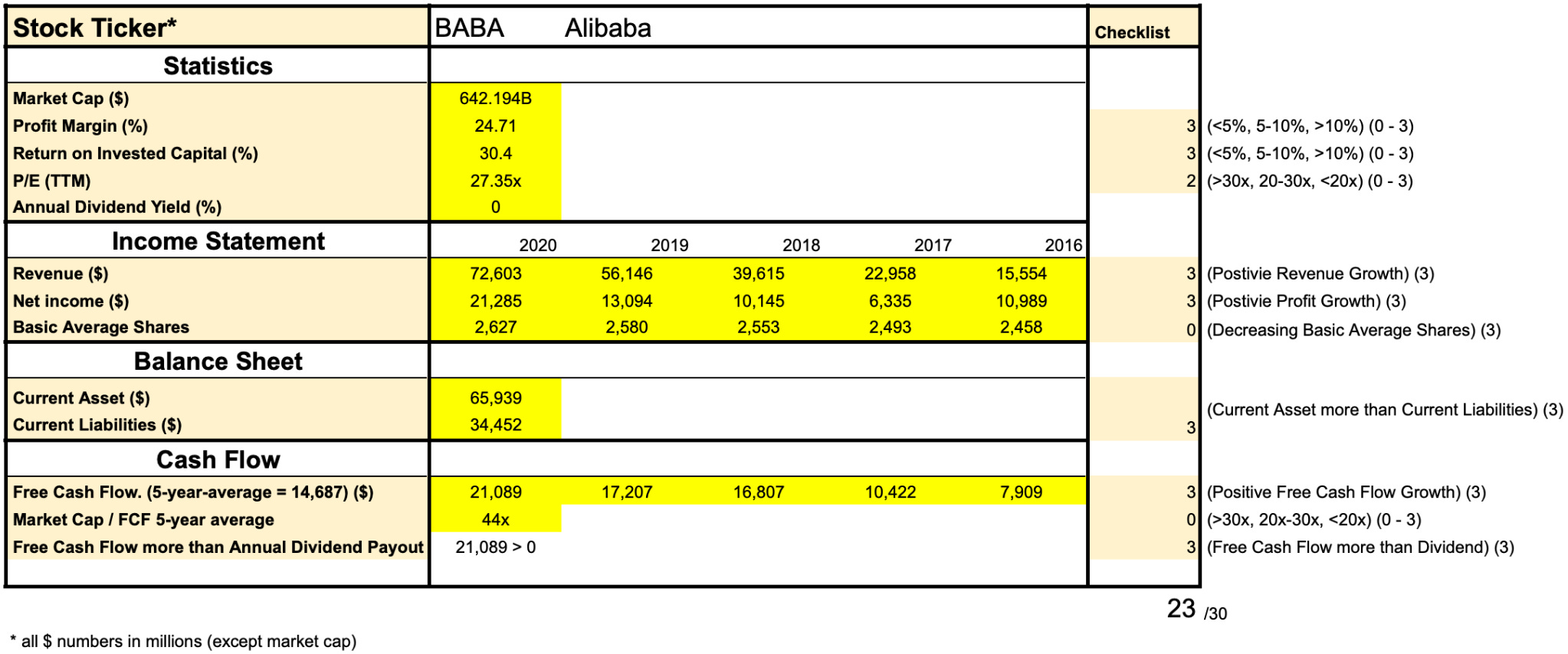

✅ First Glance at Financial Checklist

Our 10 Pillars Financial Analysis had generated a score of 23/30 for Alibaba, the highest of the three companies we had looked at so far. This score shows that Alibaba has a fantastic financial statement to back its status as a high-growth tech company. In this case, the price-earnings multiple of 27.35x will not bother me as much considering it should be able to sustain if not boost its growth for the foreseeable future. Not to mention its US rival — Amazon has a much higher P/E multiple of 81.28x just to give you a better context.

Looking into the income statement, we could spot increasing revenue and net income throughout the past 5 years. However, the company had been issuing more stocks in the past years, which makes sense given how much the stock price has surged.

The company currently has twice the amount of current assets than its current liabilities which is a plus. Also, its free cash flow had been surging exponentially throughout the past 5 years. By taking the 5-year-average of its free cash flow (5YA-FCF), we have obtained a market cap to 5YA-FCF multiples of 44x, is it ideal? I would be surprised if this company gets all checkboxes ticked, but I am happy to run with it because this a fast-growing company, and I believe there is more room for growth.

👎 What's bad?

End of China Tech’s Golden Age — Some might say the glory days for China’s technology giants are now over. The claim is not that far-fetched considering how much more aggressive the Chinese regulators had been in cracking down the monopoly practices in Chinese Big Tech lately. It started from the suspension of Ant Group’s IPO late last year, followed by the drafting of new anti-monopoly guidelines which target the country’s leading internet services, and now the overhauling of Ant Group's structure after months of discussion. Chinese big tech had been accused of monopoly practices for a while, such as the compulsory collection of user data and treating customers differently based on their spending habits, and setting algorithm-based prices favouring new users. It is only a matter of time before the government unleashes anti-monopoly regulations on the companies.

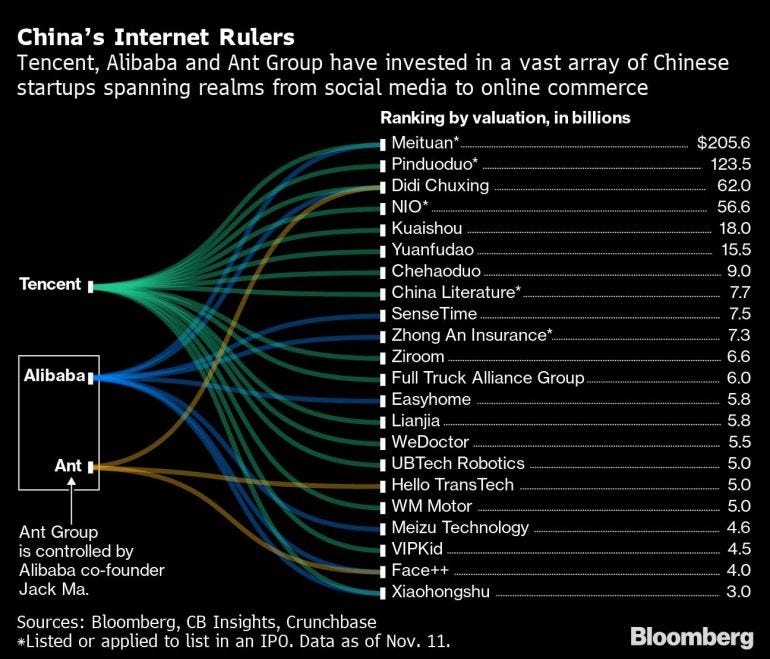

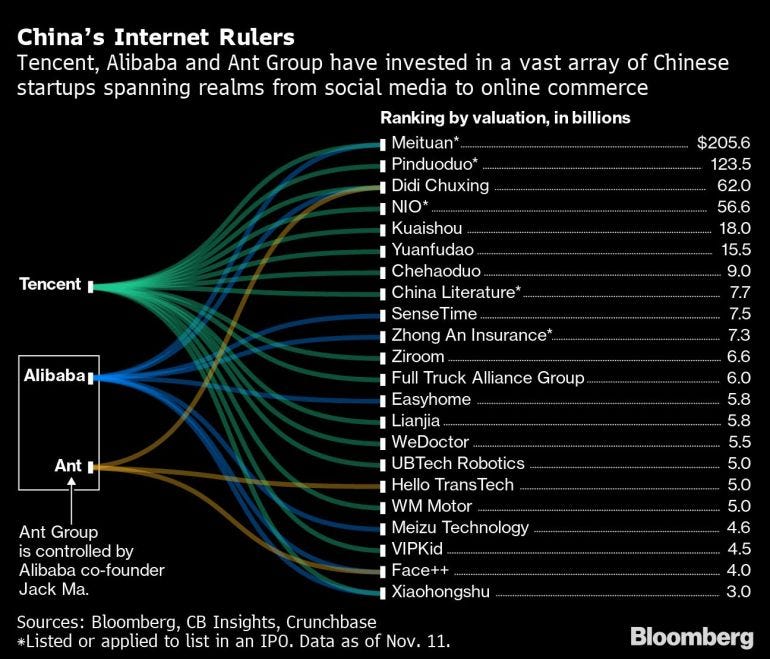

(Chinese tech giants’ connection with startups as published by Bloomberg) Concerns about getting delisted from the US stock market — The last couple of months were not exactly the best times for Chinese tech companies ever since U.S. Securities and Exchange Commission (SEC) adopted a law called the Holding Foreign Companies Accountable Act, which was passed by the administration of former President Donald Trump, basically, all Chinese companies, if get audited, there is a risk of getting delisted from the US stock market if they fail to meet strict auditing standards within three years. Sure enough, the risk remains for Alibaba even until today.

Variable interest entity (VIE) structure — For those of you who didn’t know, US investors don’t actually directly own Alibaba itself as the company was listed through a VIE structure, which means assets can be taken away without warning or compensation, as scary as it sounds, it actually happened once in Alibaba’s history when ownership of Alipay, which was a part of Alibaba was unilaterally transferred into a different company controlled solely by Jack Ma(founder and former CEO) himself. Yahoo which was a big early investor with a 43% stake in Alibaba was not informed about the transaction and nothing could be done after that due to the VIE structure itself. There are also concerns about the integrity of the company’s accounting since Chinese companies are supposedly not subjected to the same level of regulatory oversight as the US or European listed businesses.

👍 What's good?

Software vs warehouse — Unlike its biggest US rival Amazon, Alibaba does not own or rely on warehouses. It does it differently by creating a software platform that facilitates the exchange of goods and services by bringing together buyers and sellers without ever touching the merchandise (i.e. a lot like eBay). Therefore, it has higher operating margins and profit margins considering it is much easier to manage the software than building and maintaining a vast network of warehouses around the world and coordinating the packaging and delivery of orders to consumers around the globe like Amazon does.

Closure to the anti-monopoly case — After being fined $2.8 billion, the company’s Hong Kong-listed shares jumped 6.5% on Monday as it is viewed as a way of the government putting this matter behind them. Although $2.8 billion sounds like a hefty fine, it is, however, only less than 0.5% of the company’s market cap, which makes it sounds a lot like a slap on the wrist. In other words, rather than trying to destroy the company, the Chinese government is more interested in redirecting its path considering Alibaba remains a key part of China’s “belt and road” expansion in Asia.

“We are pleased that we are able to put this matter behind us”—Joe Tsai, Executive Vice Chairman, Alibaba

Fast-growing cloud business — Although cloud business generated only 8% of the company’s revenue, cloud business remains the fastest-growing sector as shown by the 50% year-over-year rise in cloud-specific revenue in Alibaba’s fiscal third quarter. The current chairman and CEO Daniel Zhang had mentioned in a 2018 interview that cloud computing will one day be Alibaba’s “main business” as the company tries to diversify its business beyond retail —just like Amazon did with Amazon Web Services more than a decade ago. Now that its cloud computing business had reported being profitable for the first time, it will be interesting to see how far the business will take off from here.

🎞 Recommended video (14 mins)

🐦 Tweets to read:

◆ What are my thoughts?

With the antitrust investigation now in the rearview mirror, I think we, as the investors, should start to shift our focus to the potential rewards ahead of us as the company focuses on growing its businesses. After all, this discount on Alibaba stock won’t last forever. At today’s price point, I think the company is still fairly undervalued. I am glad that I managed to buy more and raise the proportion of $BABA in the portfolio to 10% about a week ago when the stock was still at $225. I am very comfortable with my current investment in the company and I am going to hold the position for a very long time. Now that I have done the hardest part by buying at a dip, it is time to sit back and let the money do the work.

If you enjoy this post or Stock Investing on FIRE as a whole, please give it a ❤️ and recommend it to your friends to spread financial wellness to more people.

Best, HaoNing